Offshore wind system value after solar becomes the headline technology

TL;DR: BloombergNEF's New Energy Outlook 2026 makes a sharp claim for power-market strategy: solar becomes the world's largest source of electricity by 2032, supported by battery costs that have fallen by more than 40% since 2023. For offshore wind investors and developers, the practical consequence is clear. The offshore wind system value case now has to be evidenced, quantified and stress-tested against cheaper, faster-scaling alternatives.

Pelergy sees this as a due diligence problem rather than a messaging problem. Solar's projected rise changes how capital committees compare technologies, how developers defend grid requests, and how innovators frame the value of offshore wind technologies. Pelergy's work across LCoE modelling, cable optimisation, market entry, R&D benchmarking and the Wind Energy Technology Database gives clients a way to test that case with evidence rather than sector loyalty.

Why this matters

BNEF's article is careful about scenarios. Its economics-led transition pathway depends on currently competitive technologies. Its climate-policy transition pathway assumes stronger policy support and more difficult abatement work. Across both, BNEF describes a power system moving decisively towards solar, wind and storage.

That is a favourable macro story for renewables. It also raises the bar for offshore wind. If solar takes the global scale story, offshore wind has to win specific system roles: high-capacity coastal generation, winter output in northern markets, industrial power near ports, and strategic value where land, grid and permitting constraints limit solar buildout.

BNEF's forecast forces offshore wind to be more precise about where it creates value. A global electricity mix chart does not tell a UK, German, Baltic or US East Coast developer which project survives a grid queue, auction round, supply-chain delay or cable constraint.

What offshore wind now has to prove

Offshore wind investment papers need four tests.

First, the system-value test. A project should show how its generation profile supports the grid when solar output is lower or constrained. Capacity factor alone is too blunt; investors need dispatch value, curtailment exposure, grid connection timing and offtake logic.

Second, the delivery-readiness test. BNEF can model global capacity growth, yet individual offshore projects still live or die on ports, vessels, turbines, cables, grid works and consenting.

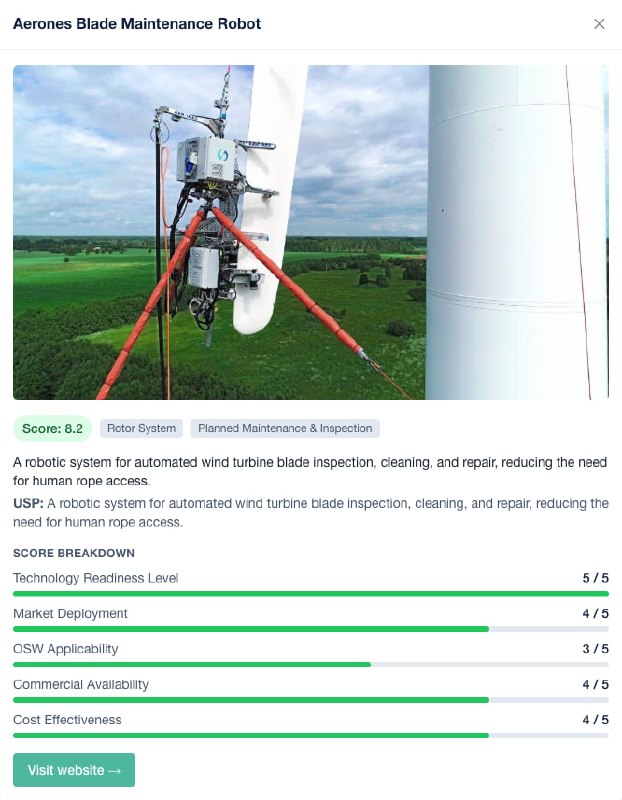

Third, the technology-readiness test. The next wave of offshore cost reduction will come from better installation methods, cable optimisation, inspection robotics and digital design tools. Those technologies need evidence tiers, reference projects and credible commercial pathways.

Fourth, the resilience test. Offshore wind still matters where policymakers and utilities need diversity in generation, industrial power supply, regional supply-chain development and long-term energy security. Those benefits need numbers attached to them, especially when the alternative looks cheaper on a headline LCoE chart.

Evidence from Pelergy project work

Pelergy has dealt with this evidence gap directly. For a crane-less turbine installation innovator, we built an investor-ready business plan using global market opportunity analysis, marine operations modelling and competitive LCoE savings logic. The value of that work was the discipline it imposed: the technology had to show where it changed installation economics, not rely on novelty.

For an AI-powered wind farm design and cable optimisation software provider, Pelergy supported corporate sales into tier-one developers. That type of tool matters more in a solar-led outlook because offshore projects need defensible answers on electrical layout, cable cost, yield and delivery risk before capital is committed.

Pelergy also benchmarked offshore wind R&D spending for a UK sector body, linking innovation investment to commercial outcomes. That work is relevant to the BNEF thesis because the sector now needs to fund technologies that improve delivery evidence, system integration and bankability.

The Wind Energy Technology Database turns that discipline into a repeatable screen. It helps developers, investors and innovators compare technology type, evidence tier, deployment fit and procurement readiness before they commit time to pilots, acquisitions or supplier conversations.

A practical decision gate for buyers and investors

Before backing an offshore wind project or enabling technology in a solar-dominated power outlook, ask five questions:

1. Which system problem does this solve that solar plus storage does not solve as well in this market?

2. Which delivery constraint has the greatest probability of delaying the project?

3. What evidence shows the technology is ready for procurement, demonstration or commercial deployment?

4. How does the value case change under lower solar and battery costs?

5. Which metric would make a capital committee change its decision?

If those answers are weak, the project needs more evidence before it needs more promotion.

Conclusion

BNEF's forecast should not push offshore wind into defensiveness. It should push the sector towards sharper evidence. Solar may become the dominant global electricity source by 2032, and offshore wind can still remain critical where grid value, industrial demand, resource quality and strategic resilience matter.

The commercial test is now harder. Developers and investors need to show where offshore wind wins in the actual system, with real constraints, real technology evidence and real delivery pathways. That is where Pelergy's diligence, market modelling and the Wind Energy Technology Database can help turn a broad energy-transition forecast into a better investment decision.

Image credit: Generated for Pelergy. Source: Generated for Pelergy.