What Wholesale CfDs could change for UK offshore wind

The UK’s proposed Wholesale Contracts for Difference scheme matters because it could change how offshore wind revenue risk is allocated between the state, generators, and the market. That has direct consequences for bid strategy, lender comfort, and how developers frame merchant exposure after the auction.

A Wholesale CfD changes the shape of the risk stack rather than clearing it away. That distinction matters for offshore wind because the market is not struggling with only one constraint. Revenue certainty is one part of the equation. Supply-chain timing, grid delivery, turbine scale, and capital discipline are still shaping whether projects move and at what cost.

Pelergy’s view is that any Wholesale CfD design should be judged on one question: does it improve investability without obscuring the real delivery constraints still sitting underneath UK offshore wind?

Why the revenue-design debate matters now

UK offshore wind has spent the past two years in an uncomfortable gap between policy ambition and project economics. Strike-price debates have dominated headlines, but the deeper issue is confidence in future cashflow under changing power-market conditions.

Developers, lenders, and equity partners all need to understand what portion of future revenue is protected, what remains exposed to wholesale-market volatility, and what assumptions still need to be carried in downside cases. When policy signals move, investment committees recalibrate.

That is exactly the kind of question Pelergy has had to unpack in adjacent market work. In a project we delivered for one client, Pelergy supported floating wind risk modelling using pipeline and leasing intelligence linked to UK market mechanisms, including CfD context. The point was not simply to count projects. It was to understand how route-to-market structure, timing, and market evidence affect commercial risk for projects moving toward scale.

That same discipline applies here. A new support mechanism only helps if it sharpens commercial visibility. If it adds complexity without clarifying revenue outcomes, it becomes another policy layer for developers and investors to interpret rather than a genuine de-risking tool.

What a Wholesale CfD could improve

A well-designed Wholesale CfD could help in three areas:

First, it could reduce uncertainty around long-term revenue capture. Offshore wind projects are capital-intensive and highly sensitive to assumptions about future price formation. If the mechanism narrows the band of merchant-risk exposure, developers may be able to present a cleaner financing case.

Second, it could improve auction confidence after the bruising reset in UK offshore wind pricing. Market participants need more than a higher headline strike price. They need confidence that the support regime reflects how power markets actually behave over an asset life that stretches far beyond the immediate policy cycle.

Third, it could help investors compare projects more consistently. In a project we delivered for a client on subsea services due-diligence, one of the critical tasks was distinguishing structural market pressure from manageable commercial risk. That required a clear view of where pricing pressure was cyclical, where it was competitive, and where capital would be needed to remain credible in the market. Offshore wind project appraisal works the same way. Better market design does not eliminate hard questions, but it can stop revenue uncertainty from contaminating every other part of the investment case.

What it will not fix

This is the part that matters most. A Wholesale CfD is not a substitute for delivery readiness.

It will not create transmission capacity. It will not shorten consent timelines. It will not guarantee vessel availability, port readiness, or supplier margin recovery. It will not make turbine scaling easier to absorb in marshalling and installation programmes.

That is why this topic should not be framed as a simple policy rescue story. Even if the UK improves revenue support design, project economics will still depend on execution realities across the supply chain.

Recent market signals make that plain and grid build-out remains a gating issue. Turbine hardware continues to scale upward. Localisation pressure is rising across Europe. All three affect cost, timing, and bankability in ways a revenue mechanism cannot fully neutralise.

For investors, that means Wholesale CfDs should be treated as one layer of risk reallocation, not a total reset of project fundamentals.

What developers and investors should watch in the detail

Three questions are worth watching closely.

How much merchant exposure remains in practice?

If the mechanism still leaves substantial uncertainty around capture prices, balancing exposure, or route-to-market assumptions, then the investability gain may be narrower than the headline suggests.

This is where the policy conversation often becomes too abstract. Committees do not approve projects on the basis of conceptual support. They approve them on the basis of a downside case they can model with confidence. If the practical revenue picture still depends on a wide range of assumptions about power prices and capture effects, the financing benefit may be more modest than the political announcement implies.

Does it improve financing clarity or add modelling complexity?

Policy reform can fail by becoming too clever. If developers and lenders need a larger stack of assumptions to understand their real downside case, the mechanism may not deliver the confidence boost it promises.

That is especially relevant in UK offshore wind, where developers are already balancing inflation exposure, procurement sequencing, and increasingly long development timelines. An elegant mechanism on paper can still create friction if it forces commercial teams to explain a more complicated risk story to lenders, boards, and investment partners.

Does it align with the physical delivery timeline of projects?

Revenue support has to be credible over the same horizon as procurement, grid connection, and installation commitments. If the policy horizon and the delivery horizon diverge, the support may look useful on paper but weak in the investment committee room.

That timing question matters because procurement choices are being made well before first power. Ports, vessels, cable packages, turbine reservations, and grid milestones all create commitments that reach far ahead of revenue realisation. If the support framework does not line up with those commitments, it will not fully unlock confidence.

Why this matters beyond fixed-bottom projects

The Wholesale CfD debate also matters because it will shape expectations well beyond today’s mainstream project set.

Floating wind, hybrid connection models, and more complex route-to-market structures will put more pressure on how policymakers describe revenue support. Pelergy’s floating wind risk modelling work showed us how quickly project risk changes when pipeline timing, leasing context, and commercial assumptions start to move together. The next wave of UK offshore wind will only intensify that need for joined-up analysis.

That matters for investors because future portfolios will not be made up of identical, low-ambiguity assets. They will include projects with different infrastructure dependencies, technology choices, and timing risk. Market design has to support that reality rather than assume a simpler market than the one developers are actually building into.

The Pelergy view

The most useful outcome would be a market design that reduces avoidable revenue ambiguity while leaving no illusions about the physical constraints still shaping offshore wind delivery.

A stronger revenue mechanism can improve bankability. Supply-chain planning, grid coordination, and commercial diligence still have to do the rest.

This is also where next-generation project assessment will matter more. As offshore wind portfolios become more exposed to larger turbines, floating pathways, evolving grid architecture, and mixed merchant-support models, diligence has to become more integrated. Revenue design, infrastructure readiness, and technology choices can no longer be analysed in isolation.

That is a commercialisation question as much as a policy one. The winners will be the teams that can translate changing market structures into credible project strategies before those changes are fully priced in.

What this means for Pelergy clients

For developers, the immediate task is to test whether a Wholesale CfD would materially change bid behaviour, financing conversations, or procurement timing.

For investors, the task is slightly different. It is to separate the part of the opportunity that is genuinely being de-risked from the part that still depends on execution capability and market discipline.

Pelergy helps clients do exactly that: map the real operating implications behind market signals, pressure-test assumptions, and connect policy movement to investable delivery decisions.

If you are assessing how changing UK market design affects offshore wind strategy, Pelergy’s market intelligence and technology diligence work can help.

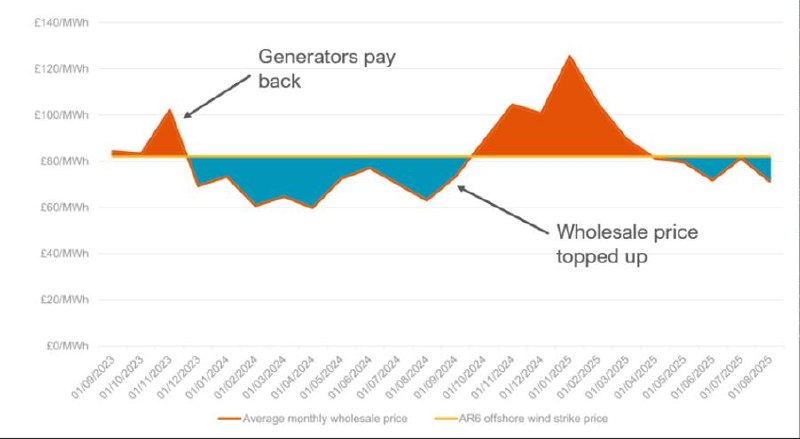

Image credit: Energy UK. Source: Energy UK.